States with No Income Tax: A Complete Guide for Retirees

Decisions you make in retirement significantly affect how long your money lasts, including how much of your income goes to taxes. While tax implications most certainly shouldn’t determine where you spend your golden years, this oft-overlooked consideration can have significant implications for your retirement.

This guide explores the nine states lacking income tax, how they treat different types of retirement income (including Social Security, pensions, and IRAs), trade-offs, and real-world examples of how the numbers play out: giving you a clearer picture of whether a no-income-tax state is financially advantageous for your retirement years.

- Nine states levy no broad income tax — a meaningful draw for retirees on a fixed income.

- These states don’t tax Social Security, pensions, or retirement-account withdrawals at the state level.

- The revenue shifts elsewhere — often to higher sales taxes, property taxes, and fees.

- Weigh the full picture — cost of living and healthcare can outweigh the tax savings.

Are states with no income tax better for retirees?

While states with zero income tax might seem like a financial paradise—offering the chance to keep more of your hard-earned money—complex factors are indeed in play as they are with most financial decisions. Such states may relieve retirees of income tax, for example, but they often bring in money from residents in other ways (e.g., higher property taxes, sales tax, or related fees). Other factors like healthcare, cost of living, and quality of life all come into play as well.

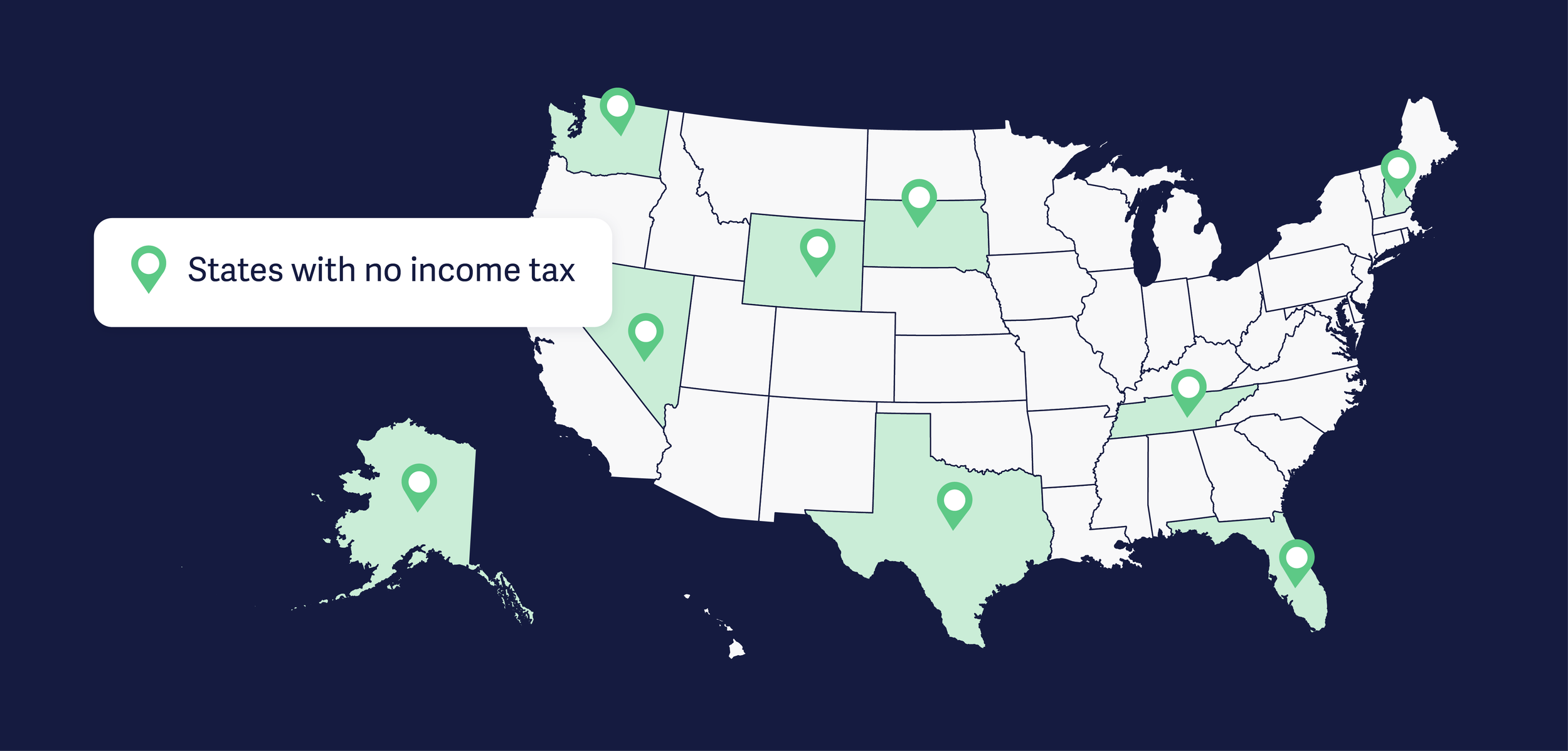

Which states have no income tax?

Let’s start with the nine states that don’t levy a broad-based state income tax:

Alaska

Florida

Nevada

South Dakota

Tennessee

Texas

Washington

Wyoming

New Hampshire

In these states, income from wages, pensions, IRAs, and 401(k) withdrawals is free of state-level taxes.

Why state income tax matters in retirement

Anyone earning income can potentially benefit from not owing state income taxes, but the advantages are especially noteworthy for retirees living on a fixed income. It’s also worth noting that retirees often enjoy more geographic flexibility than those still working since they’re no longer tied to a specific location for a job (with any children likely out of the house by this point). As for the numbers themselves, consider this example…

Imagine two retirees who each bring in $60,000 in annual income: $30,000 from Social Security, $20,000 from IRAs, and $10,000 from part-time consulting work. If one lives in Texas, his or her state tax bill would be a big fat $0. Should the other live in California or New York, for example, that person would be staring down several thousand dollars in annual state income taxes—the difference between the two easily amounting to somewhere between $50,000 and $100,000 over the course of a 20-year retirement.

It's no wonder relocating to a no-income-tax state for retirement is tempting, but soon-to-be retirees must carefully analyze the entire financial picture before making any decisions.

How Social Security is treated

Social Security benefits are a lifeline for millions of retirees, often comprising the largest portion of retirement income. At the federal level, up to 85% of benefits can be taxable depending on combined income. Rules vary by state, but the good news is no-income-tax states don’t tax Social Security at all—important for retirees on a tight budget as keeping every dollar of these payments can make a substantial difference.

Pensions, IRA withdrawals, and investment income

How No-Income-Tax States Treat Retirement Income

State-level treatment in the nine states without a broad income tax.

| Income type | Treatment at the state level |

|---|---|

| Social Security | Not taxed |

| Pensions | Fully exempt |

| IRA & 401(k) withdrawals | You keep the full amount, aside from federal tax |

| Investment income (interest, dividends, capital gains) | Not taxed at the state level |

State-level treatment only. Federal tax still applies — for example, up to 85% of Social Security benefits can be taxable federally depending on your combined income. This is general information, not tax advice for your specific situation.

While Social Security is safe from state taxation in no-income-tax states, pensions and withdrawals from retirement accounts are where these states really shine.

Pensions

In many income-taxing states, pension income is taxed as ordinary income (though some states offer partial exemptions). In no-income-tax states, pensions are completely exempt.

IRAs and 401(k)s

Withdrawals are treated like income in most states that levy an income tax. In no-tax states, residents keep the full withdrawal amount (aside from federal tax obligations).

Investment income

Interest, dividends, and capital gains are not taxed at the state level in most no-income-tax states: with the potential for significant accumulation among retirees who’ve saved diligently and expect to rely heavily on their portfolios.

Trade-offs: what you give up

No income tax doesn’t mean no taxes

States without an income tax still need revenue, so they usually make it up elsewhere — higher sales taxes, higher property taxes, and various fees. If you spend heavily on taxable goods or own a high-value home, those costs can offset some or all of your income-tax savings.

No-income-tax states don’t simply wash their hands of revenue and instead often shift the burden elsewhere, meaning retirees moving to one of these states should prepare themselves for potential trade-offs such as…

Higher sales tax

Many no-income-tax states lean heavily on sales tax to fund government services. Tennessee, for example, has one of the highest combined state and local sales tax rates in the nation with a 7% base state sales tax and up to 2.75% additional in local sales tax—adding up to only a hair shy of 10% in many parts of the state. Washington is similar, with a state sales tax of 6.5% and additional local sales tax known to total above 10% in this case. The key takeaway? Higher sales tax may offset any income tax savings if you spend a lot on taxable goods and services.

Higher property taxes

Another way no-income-tax states shift the burden is via higher property taxes. Take Texas, for example, where homeowners face some of the highest property tax rates in the U.S. While you may save thousands on income tax, your home could leave you with a hefty annual property tax bill: an important calculation for retirees who own property.

Fees and other taxes

Some no-income-tax states raise revenue through higher licensing fees, gasoline taxes, or “sin” taxes on items like alcohol and tobacco.

Cost of living

Of course, taxes are only part of the financial equation. Housing, healthcare, and insurance can vary dramatically from one state to another or even within each state. While Florida’s lack of income tax is attractive, rising housing costs in popular areas may eat into those savings. States like Wyoming, meanwhile, may offer a lower cost of living overall but lack easily accessible healthcare or amenities in some areas.

Case studies: how the math works

Taxes are incredibly complex. In order to get a general idea of potential financial implications when it comes to living in a state with no income tax, let’s consider two hypothetical case studies.

Case study 1: Mary

After moving from Oregon to Florida for retirement, Mary receives $24,000 annually from Social Security and withdraws $16,000 from her IRA. In Florida, her annual state income tax bill is $0 versus the $1,000+ she’d owe had she stayed in the Pacific Northwest: a $20,000 difference over 20 years! Mary’s move also gifted her a lower cost of living, in large part due to more affordable housing.

Case study 2: John

John, meanwhile, has $30,000 in Social Security, $40,000 in pension income, and $20,000 in investment income. He lives in California but is considering a move to Texas now that he’s retired, in part, due to potential tax savings. In Texas, he’d pay nothing at the state level but could owe $4,000 to $6,000 annually in state tax in California (depending on brackets): $100,000 to $150,000 in additional costs over a 25-year retirement, potentially. John also owns his home and is interested in purchasing rental properties, potentially eating into his tax savings in Texas given higher property tax rates than California.

State-by-state tax highlights

The Nine No-Income-Tax States at a Glance

High-level draws and trade-offs for retirees, as covered in this article.

| State | Draw | Trade-off to weigh |

|---|---|---|

| Florida | Moderate cost of living; healthcare geared to retirees | Coastal housing can be pricey |

| Texas | Moderate cost of living; solid metro healthcare | Steep property taxes |

| Tennessee | More affordable housing than coastal states | Among the highest sales tax in the country |

| Washington | Strong healthcare and cultural amenities | High sales tax and cost of living, especially Seattle |

| Wyoming | Low property and sales taxes; low cost of living | Limited healthcare outside larger towns |

| Alaska | No income tax; residents receive an annual oil-revenue dividend | High cost of living, isolation, harsh climate |

| Nevada | Relatively low property taxes; warm climate | Healthcare limited outside major cities |

| South Dakota | Low taxes overall; affordable cost of living | Harsh winters; limited rural healthcare |

| New Hampshire | No state income tax of any kind (its former tax on dividends and interest was repealed effective 2025) | Property taxes among the highest in the U.S. |

Cost-of-living and healthcare notes are general and vary by area within each state. This is general information, not tax advice for your specific situation.

Where exactly you choose to settle down in a state can have an impact too since rural areas typically offer a lower cost of living than cities. Local taxes also vary—meaning the effective tax rate in one county may vary from that of another—with weather and other related factors in the mix as well from state to state (admittedly having nothing to do with taxes but still important nonetheless). With this in mind, here are some high-level considerations for each of the nine income-tax-free states.

Florida

Famous for sunshine, retirees, and a relatively moderate cost of living (though coastal housing can be pricey)

A healthcare infrastructure that caters to retirees

Texas

Steep property taxes, though the cost of living is moderate

Solid healthcare options in metro areas

Tennessee

Among the highest sales tax in the country

More affordable housing compared to coastal states

Washington

High sales tax and cost of living (especially in Seattle)

Robust healthcare and cultural amenities

Wyoming

Low taxes, including property and sales taxes, and a relatively low cost of living

Potentially limited healthcare access outside of larger towns

Alaska

No income tax, with residents paid an annual dividend from oil revenues in fact

Deterrents include a high cost of living, potential for isolation, and harsh climate

Nevada

Relatively low property taxes

Popular with retirees for its warm climate, though healthcare resources may be limited outside of major cities (e.g., Las Vegas or Reno)

South Dakota

Low taxes overall and an affordable cost of living

Harsh winters and limited healthcare access in rural areas

New Hampshire

No income tax; its former tax on dividends and interest was repealed effective 2025

Property taxes among the highest in the U.S.

Beyond taxes: quality of life factors

While taxes are a major consideration, retirees shouldn’t overlook what their lifestyle will look like in the place they choose to settle down. With access to good healthcare, climate preferences, proximity to family, cultural amenities, and recreational opportunities all impacting whether a state is a good fit, it’s important to assess things like these knowing the best retirement destination is one balancing financial advantages with personal needs and preferences.

The takeaway

States with no income tax can deliver big financial advantages—especially for retirees—but sales, property, and other taxes can offset income tax savings (with cost-of-living differences also known to widely vary). If you’re considering a move to a no-income-tax state, work with a financial advisor to understand the full tax and cost-of-living picture; what looks perfect on paper may feel less so in practice. Ultimately, the best retirement state is the one providing a comfortable, affordable, and joy-filled lifestyle in your golden years.

Still unsure about your own situation? Consult with one of our tax professionals who can review your circumstances in detail, knowing a little planning can go a long way toward reducing your tax burden and making retirement more affordable. We’d love to hear from you at 201-488-2828 or support@kaleedscpa.com.

Disclosure:

This article is for general informational purposes only and is not intended as tax or legal advice. Please consult a qualified professional regarding your individual situation.