How Bonuses Are Taxed (and How to Keep More of Yours in 2026)

You finally got that long-awaited bonus—but then you see your paycheck. Where did it all go? It’s not just in your head; bonuses are taxed differently than regular pay, meaning your reward can look smaller than what you expected since the IRS considers bonuses “supplemental wages” that come with their own withholding methods and rates. Don’t panic! Your money didn’t disappear into thin air. Here’s how bonus taxes actually work and what you can do to keep more of your hard-earned money next time.

Why bonuses are taxed differently than regular paychecks

It’s easy to assume a bonus should be taxed just like a normal paycheck; income is income, right? Not exactly. Bonuses show up with regular wages on your W-2. If you’ve withheld enough, great! If not, you’ll either see a refund or small bill come tax time.

When it comes to payroll, the IRS puts bonuses into a special category called “supplemental wages”—a term covering any extra pay you earn on top of your regular salary—for things like commissions, overtime, or severance pay. Because these payments are often one-offs or irregular, the IRS has special rules for how employers handle withholding.

Here’s what that means in practice. Rather than using your usual tax rate, your employer follows specific IRS guidelines to calculate how much to withhold from your bonus. The goal? To ensure enough tax is paid upfront even though your total tax bill will depend on your overall income for the year. This can make your bonus look smaller at first, but it doesn’t necessarily mean you’re being taxed more.

It really comes down to timing since your employer is technically just prepaying a chunk of your taxes on your behalf. Everything evens out when you file your return, and you’ll get some of it back as a refund if too much was withheld.

Two employer bonus tax-withholding strategies

Employers typically have a pair of options for how to withhold federal income tax, the method chosen making a big difference in how much shows up in your paycheck (at least at first glance).

The percentage method

The percentage method is the most common (and simplest) approach whereby your employer treats your bonus separately from your regular paycheck and withholds a flat 22% for federal income tax. If you’re lucky enough to receive a larger bonus (e.g., more than $1 million) the first million is still taxed at 22% with anything above that withheld at 37%—the current top federal rate. This makes it easy for both employers and employees to see what’s coming out right away, but it can also mean withholding doesn’t perfectly match your actual tax bracket (leading to a refund come tax time or the opposite whereby you’ll owe a little more, depending on your full year’s income).

The aggregate method

Some employers combine bonuses with regular paychecks and withhold taxes based on an employee’s normal income rate, typically when both are paid together in a single check. Using this method, your employer calculates the total amount (regular pay + bonus), applies your usual tax rate, and withholds accordingly. This can make your bonus look more heavily taxed if you’re in a higher tax bracket despite your overall tax liability perhaps not changing.

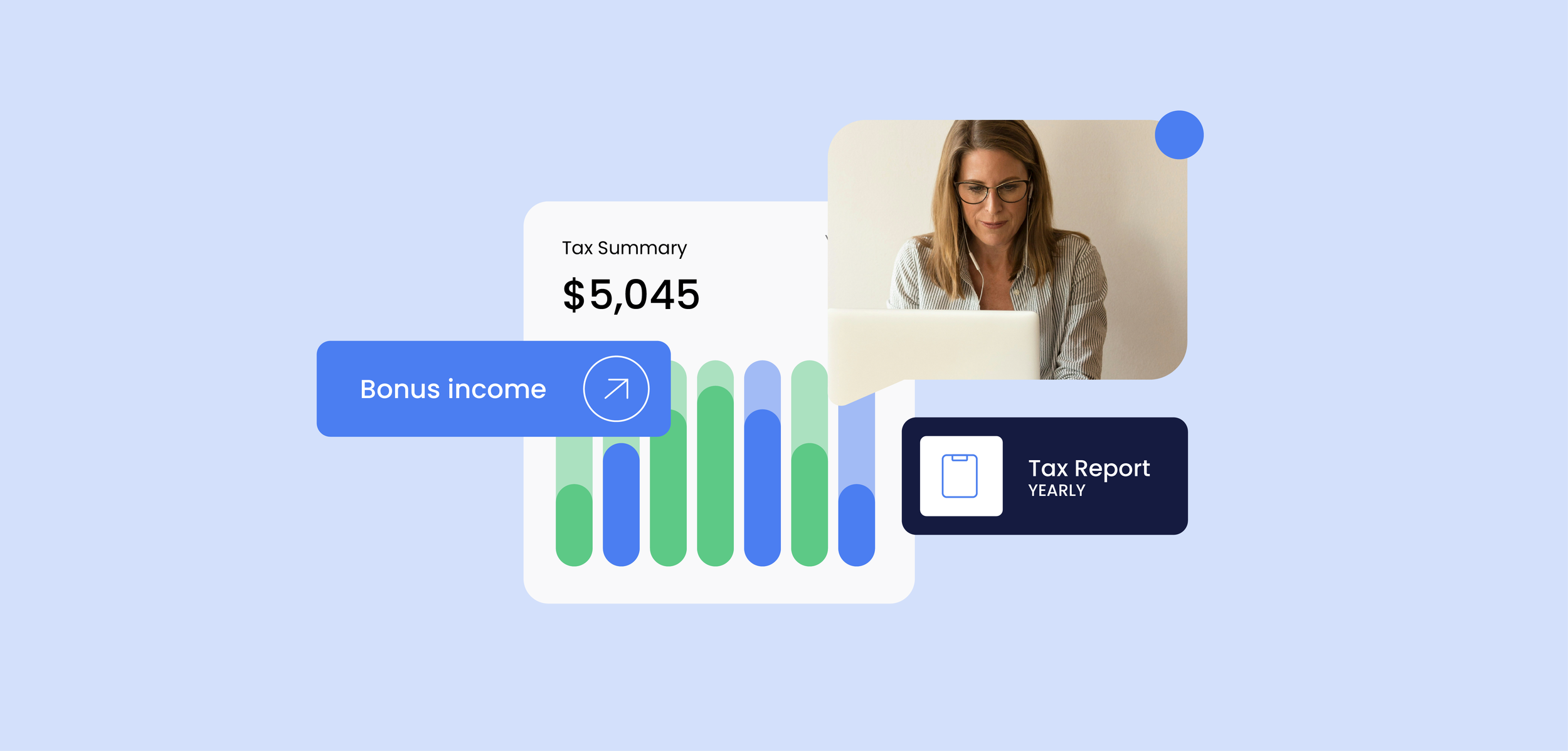

Example

Consider a $5,000 bonus.

Employers using the percentage method will withhold 22% (or $1,100) for federal income tax, resulting in a $3,900 paycheck (before other taxes like Social Security and Medicare).

Employers using the aggregate method for someone in a 32% bracket (for example) means a combined paycheck withholding $1,600 and less money upfront ($3,400).

Either way, you’re not being “double taxed.” When you file your return, your total income and actual tax bracket determine what you really pay.

Federal vs. state taxes on bonuses

Your bonus doesn’t just face federal withholding but is also subject to the same payroll and state taxes as your regular paycheck. Here’s how it all breaks down:

Federal income taxes

Federal tax rates will remain between 10% and 37% through 2026, with income thresholds and standard deductions rising slightly each year thereafter to keep pace with inflation. With your employer withholding 22% (or 37% for bonuses over $1 million) as an estimate, your bonus is combined with your total income and taxed at your actual rate when you file your return—which may mean a small refund or balance due at tax time.

State income taxes

Most states tax bonuses the same way they tax regular wages, but the withholding rate varies depending on where you live.*

· States with a flat income tax: A handful of states apply one uniform rate to most income, meaning everyone pays the same percentage regardless of income level.

· States with progressive income tax: Most states use a tiered system, taxing higher income levels (including bonuses) at higher rates.

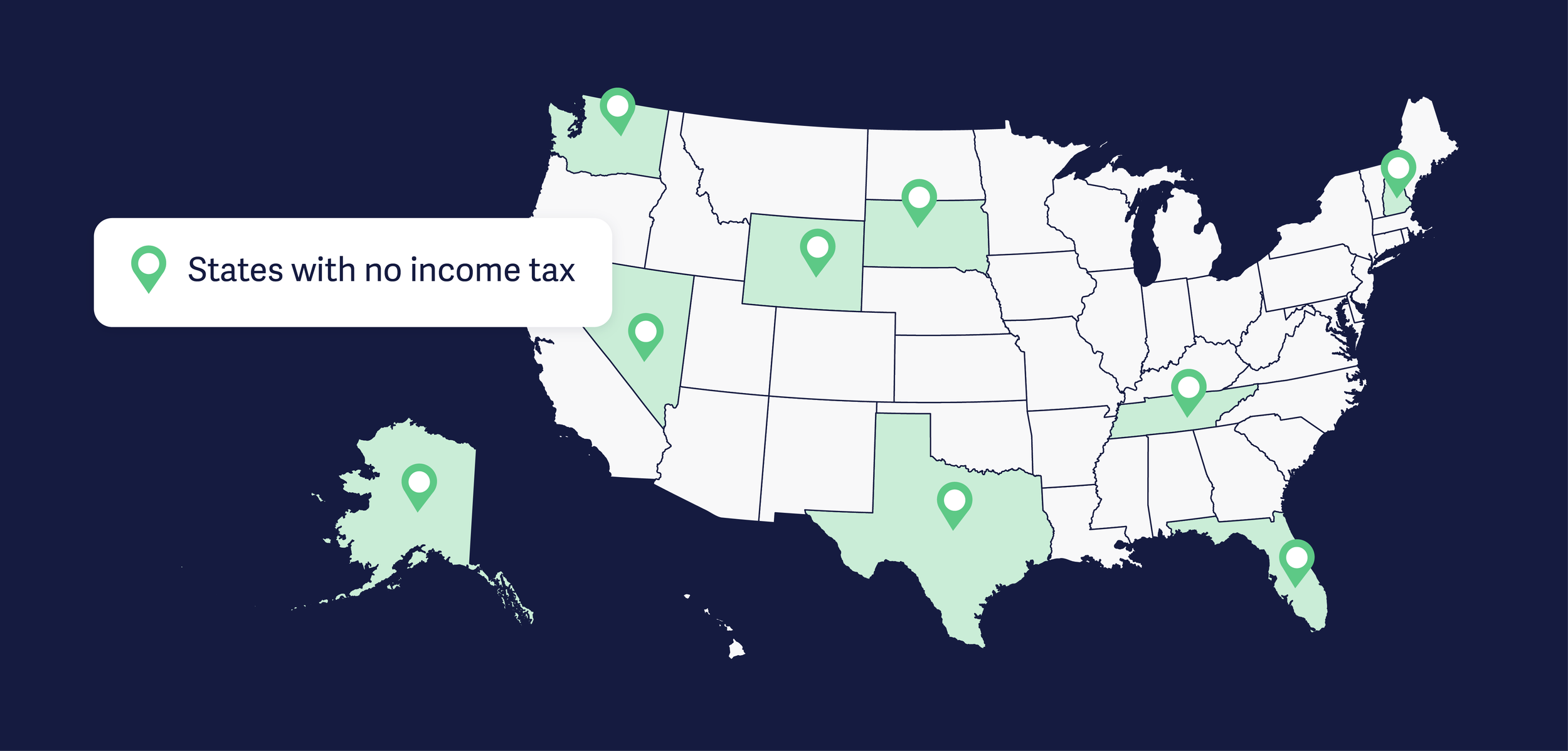

· States including Alaska, Texas, Nevada, New Hampshire, Tennessee, South Dakota, Wyoming, Florida, and Washington** have no state income tax, meaning bonuses only face federal and payroll taxes.

*Check your state revenue department or employer payroll portal for exact rates applied to bonuses since state rules differ.

**Washington doesn’t tax income but does tax capital gains for some high earners.

Social Security and Medicare taxes

No matter where you live, bonuses are also subject to FICA (Federal Insurance Contributions Act) taxes:

Social Security: This is 6.2% on wages (including bonuses), up to the 2025 wage base of $176,100, with the Social Security Administration projecting this cap will rise to ~$183,300 in 2026—meaning high earners will see slightly higher withholding next year (up to ~$11,364).

Medicare: This is 1.45% on all wages with no cap, plus an extra 0.9% surtax for high earners ($200,000 for single filers; $250,000 for joint filers).

These payroll taxes are automatically withheld and separate from federal income-tax withholding. While they may shrink your bonus check a bit more, they’ll at least fund your future Social Security and Medicare benefits.

4 bonus tax-reduction strategies

While you can’t avoid bonus taxes altogether, a few smart strategies can help bring down the amount owed or at least make the tax bite sting a bit less. These include…

1. Contributing to your 401(k), IRA, or HSA

One of the easiest ways to reduce your taxable income is to funnel a portion of your bonus into a tax-advantaged account.

As 401(k) contributions come straight out of your paycheck before taxes, putting more of your bonus toward retirement savings can immediately shrink your taxable income.

Traditional IRA contributions can also reduce taxable income if you qualify for a deduction.

If you’re enrolled in a high-deductible health plan, contributing to a health savings account (HSA) allows you to set aside pretax dollars for medical expenses as a triple tax benefit that can stretch your bonus even further.

2. Asking to defer your bonus

Think you’ll earn less next year? You might be able to defer your bonus until then, potentially dropping you into a lower bracket and shrinking your tax bill.

3. Making charitable donations or deductible payments

Donating a portion of your bonus to a qualified charity can lower your taxable income if you itemize. You can also plan deductible expenses (e.g., medical costs) in the same year to maximize your deductions.

4. Planning ahead with HR or a tax professional

Check in with HR or a tax pro before your bonus hits; they can walk you through tax withholding and help fine-tune your W-4 so you’re not caught off guard when it’s time to file.

Are all bonuses taxable?

In most cases, yes. If it feels like income, the IRS treats it as such. The type of bonus you receive, however, can impact how (and whether) it’s taxed.

Cash and cash equivalents

Any cash bonus you receive, whether a direct deposit or paper check, counts as taxable income. This applies even to gift cards in most cases because the IRS considers these a cash equivalent—meaning if your company gives you a $200 Visa gift card for a job well done, it’s treated the same as receiving $200 in your paycheck.

Noncash gifts and perks

Freebies like event tickets, merchandise, meals, or company swag often fall into a gray area as many are considered “fringe benefits.” The IRS decides whether these are taxable based on their value and how often they’re awarded. While small, occasional items (e.g., coffee mugs and T-shirts) are typically considered de minimis benefits—meaning they’re too minor to tax—bigger or more frequent perks such as concert tickets, paid trips, or luxury gifts are usually taxable and must be reported as income.

Achievement awards

Special achievement awards (related to safety milestones or years of service, for example) are sometimes partially tax-free but only if they meet certain criteria. The award must be tangible (think trophies) and part of a qualified employee-recognition program. Cash or gift cards, even for achievements, don’t qualify.

Unsure whether a perk or prize is taxable? It’s safest to assume it is or otherwise simply double-check with HR before tax season.

When and how bonus taxes are paid

How the process plays out:

1. Your employer withholds taxes upfront. As we discussed previously, bonuses are considered supplemental income so employers usually withhold 22% for federal income tax (or 37% if your total supplemental pay for the year exceeds $1 million).

2. Payroll taxes are also deducted. Social Security, Medicare, and any applicable state income taxes are withheld just as they are from your regular paycheck.

3. Funds go directly to the IRS and other tax agencies. Your employer sends the aforementioned money on your behalf, with taxes paid in real time.

When you file your tax return:

1. Your bonus is added to your regular income and reported in Box 1 of your W-2.

2. The IRS calculates your actual tax based on your total annual income and tax bracket.

3. If too much was withheld, you’ll receive a refund.

4. If not enough was withheld, you’ll owe a balance come tax time.

Bonus withholding is just an estimate, with the final number evening out when you file your return and the IRS compares what you owe to what you’ve already paid.

The bottom line about your bonus taxes

Taxes on bonuses are often confusing but easier to manage once you know how they work. Keep an eye on your withholdings, especially if you expect a big payout or change in income, and don’t be afraid to tweak your W-4 if needed. The goal is to make sure your hard-earned bonus ends up where it belongs: in your pocket.

Want to speak with a tax professional to receive personalized advice? Reach out to us at 201-488-2828 or support@kaleedscpa.com.

Disclosure:

This article is for general informational purposes only and is not intended as tax or legal advice. Please consult a qualified professional regarding your individual situation.